Private Credit's AI Problem

Plus: Welcome back, Trevor Milton

Welcome to Young Money! If you’re new here, you can join the tens of thousands of subscribers receiving my essays each week by adding your email below.

Hello there, and happy Monday to those who celebrate.

I am, to the best of my abilities, trying to work back into writing this thing weekly. Beyond the fact that 1) I enjoy writing and 2) this newsletter is probably the most valuable asset I have to my name, Young Money serves as a good forcing function for me to put my thoughts on the world around me into writing. Plus, “AI brain” is 100% a thing (I’ve felt it!) and I do think regular writing is more important now than ever before as forced cognitive exercise.

I’ve also done a bit of thinking on the format here, and I do think the “right” setup is a mix of riffs on my life + my thoughts on whatever tech/market/investing trends seem most relevant, since that is 1) what I’m interested in and 2) where I spend most of my time working / reading. So let’s get started.

A few thoughts on the internet, serendipity, etc.

I’ve written this newsletter for, something like, five years now. I think I put out my first piece in June 2021 explaining how it was structurally impossible for bitcoin to simultaneously be an “inflation hedge” and a “currency.” I was right, but didn’t matter. It turned out to be a fantastic risk asset despite it still sucking as a medium of exchange. Whatever. Anyway, I’ve written like a million words since then, and downstream of those words have been a fantastic stream of new connections and friendships. Yapping on the internet, it turns out, is a really good way to attract people you’d probably like hanging out with.

Yesterday I hung out with a new internet connection-turned IRL friend Pilar Brito. She’s an attorney-turned wine creator (IG here, Substack here) turned startup operator who just moved to NYC. We ended up drinking wine at Fedora for like 3 hours. Great place; highly recommend. Pilar is also one of our panelists at Slow Ventures’ Etiquette School in NYC next Tuesday (more on this at the bottom of the newsletter) where she’ll be discussing everything you didn’t need to know about wine. We met through some combination of my newsletter, the Etiquette School we hosted in San Francisco last fall, and a bunch of the Creator stuff we’ve been doing at Slow; it was a fresh reminder that, yes, putting yourself out there online is such a ridiculous serendipity machine and I should get back into it. Also, orange wine is great. But more on that next Tuesday at Etiquette School.

Okay, some thoughts on private credit:

Private Credit / AI Doom Loop:

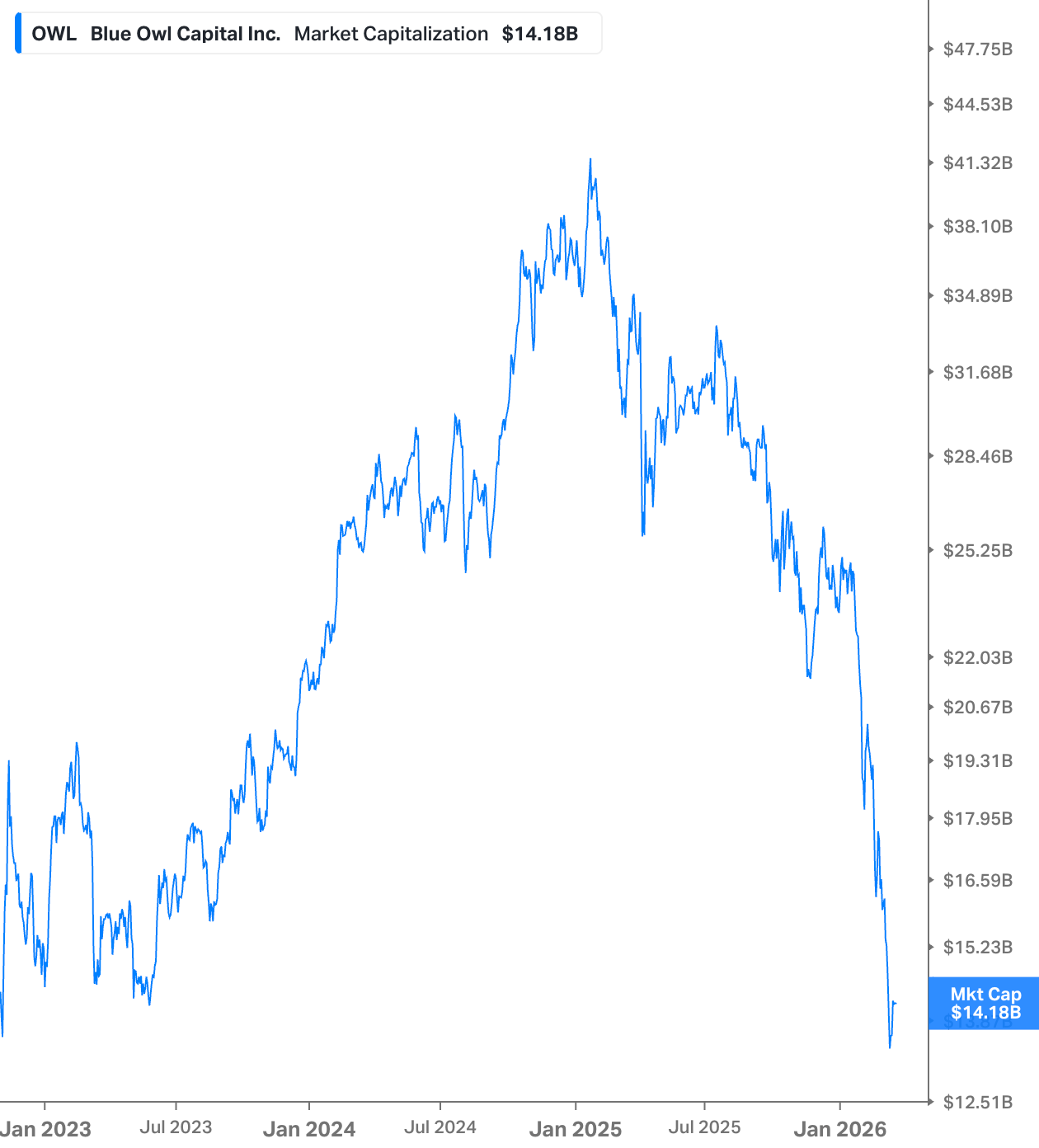

Blue Owl is an “alternative asset manager” that manages ~$307 billion, with ~$158 billion going toward private credit, and $115 billion of that in direct lending. You know how you can go borrow money from the bank to buy a house (aka a mortgage)? Well, Blue Owl, among other things, similarly lends money to companies, and Blue Owl makes money by charging their investors somewhere between 1.25% and 1.50% on their AUM, + incentive fees in the form of a slice of the net interest income generated from their loans.

When you make money from fees, your revenue jumps with your AUM. Blue Owl’s AUM at the end of 2022 was $138 billion. Its revenue was ~$1.4 billion. Blue Owl’s AUM at the end of 2025 was $307 billion. Its revenue for 2025 was ~$2.9 billion. Wall Street, for a couple of years, rewarded this AUM and revenue growth with a soaring stock price as Blue Owl’s market cap cruised from ~$15 billion to ~$40 billion from November 2022 to January 2025.

Then the stock collapsed, now back down to a ~$14 billion market cap since peaking early last year.

What happened? Investors are losing trust in private credits’ “marks.” Again, private credit funds primarily make money by charging fees on their AUM. To make more money, they want to grow assets, which means loaning more money to more companies. But if the value of those loans declines? Then so do fees and profits for the firm.

You may have heard of Claude Code. It’s pretty cool; you can just tell your computer, in English, to build some software, and it can, with some guiding, do it. Random things I’ve built with Claude Code in the last year or so:

A personal assistant, named “Clank,” that I chat with through Telegram who can edit Github repos, access and navigate my rolodex, make phone calls for me, email folks, etc.

A few different personal organizational tools that consolidate and summarize meeting transcripts, email threads, etc.

An automated newsletter digest podcast that takes newsletters I flag as “podcast material” and transcribes the content to audio format, then publishes a private podcast for me to listen to any interesting newsletters I lack time to read.

An automated email translation tool that translates any newsletters I forward to a specific email address into Spanish, then sends them back to me.

Coding assistants last summer sucked. They “worked,” but needed to be hand-held to build anything even remotely useful. In December, around the time Anthropic and OpenAI released their new models, coding assistants suddenly became “good.” Like, you give it a task, go cook dinner, come back, and you have a fully-functioning web app good. A lot of investors worry now, for good reason, that a lot of software companies might be a lot less valuable than they were six months ago.

Some software only exists to give humans a good interface through which they can interact with their data. AI tools don’t need “interfaces” to interact with data; they just need APIs. And with the costs of software creation (or, at least, code generation) plummeting to zero, there’s a real possibility that some previously-bought software tools can now be created internally. I don’t buy the argument that anyone is going to “vibecode a Salesforce” any time soon, but even the possibility of building an alternative to parts of your internal software stack hurts the pricing power of software vendors. Pre-AI coding assistant, you might expect to hike your prices by ~5% a year because of course you can. That’s just how pricing increases worked. But now? You have to work a lot harder to maintain customers who think they could, with some effort, build their own replacement if they’re feeling overcharged.

So now what? You, the software vendor, might make less money. Your margins compress. Maybe a creditor had loaned you $100m in 2023 when your EBITDA was $20m and you looked poised for rocket ship growth, but now your customers think they can vibe code half of your functionality and they’re considering cancelling their contracts. You offer them a big discount to stay on platform, but the contract drops from $500,000 to $425,000 in a year that you had otherwise expected to charge $525,000. This happens to a lot of customers. Suddenly that $20m in 2023 EBITDA is $14m in 2026. Interest coverage is getting hairier. The assumptions you made in 2023 got blown up by Claude, and now those loans are worth as much as you thought they were. The market wants higher yield for that risk, and the value of those loans declines. If the value of your loans declines, your AUM declines, you make less in fees.

That stock price collapse? It’s the market saying it doesn’t trust a lot of these private credit marks anymore.

Blue Owl has several funds, including an unlisted (private) Blue Owl Capital Corporation II (OBDC II) and a publicly-traded Blue Owl Capital Corporation (OBDC). OBDC II had a cap on quarterly redemptions set at 5% of NAV; throughout 2025, they kept hitting that cap as investors wanted to get out. Blue Owl thought it had a solution to give more investors liquidity: merge the private fund with their publicly-traded OBDC, giving the OBDC II investors 1:1 shares in the public entity for their shares in the private fund. There was just one issue: while the shares of OBDC II were still supposedly worth around their par value, the public vehicle was trading at a 20% discount to its NAV, meaning the market didn’t think the loans were worth what Blue Owl said they were worth. Had the merger gone through, the investors in the private fund would have likely taken a 20% markdown on their investments as well. Investors, were, obviously, pissed. No one wants a 20% markdown.

Blue Owl instead sold $1.4 billion worth of loans, including $600 million from OBDC II, to raise cash to return capital to their investors at close to par value. Very nice of them. It doesn’t fix the core issue that, while they’re returning capital at “par” in the near-term, the market doesn’t trust their marks now, and some other investors don’t either:

Boaz Weinstein’s Saba Capital offered to buy investors’ stakes in OBDC II at a 20-35% discount to NAV for any investors who want liquidity. TLDR: the market increasingly doesn’t think these private credit loans are “worth” what the funds claim they’re worth. You can say your NAV is whatever you want, but the price of anything is only what someone else will pay for it.

Blue Owl isn’t the only private credit lender with growing pains, either. Last week, Nick Nemeth wrote a great piece calling for increased transparency on private equity and private credit valuations, calling out private credit fund Cliffwater for almost-certainly mis-stating its loan book. Unreported payment-in-kind (PIK) loans (meaning that, instead of paying back interest in cash, interest is “paid” by accruing more debt on the principal of the loan), marking up loan valuations when the rest of the loan market fell on Liberation Day, claiming a 41-month win streak despite all of the volatility in the lending market in the last year. It’s just basically impossible that Cliffwater’s loans are worth what they claim they’re worth.

Fine. Whatever. Private credit is “overly optimistic” about some of their loans, and maybe they’ll take some haircuts on those loans as their borrowers lose customers who vibe-coded their SaaS solutions instead of renewing contracts. Who cares that a few MDs lose out on their carry checks because their funds underperform? Well, the irony here is that the same folks dishing out private credit loans to SaaS sellers are financing the datacenter buildout that’s fueling the AI models that are threatening to kill the same SaaS apps they also lended to.

Guess who partnered with Meta on its ~$27 billion “Project Hyperion” datacenter buildout in Louisiana? Blue Owl, the same fund whose stock has collapsed over the last year. Blue Owl created an SPV called “Beignet Investor LCC” (which is, objectively, a hilarious name for a Louisana-based datacenter project) through which it raised $27.30 billion (on top of $2.45 billion in equity contributions itself) to finance this datacenter buildout. Meta is contributing the other ~20% of costs. Cool. Meta’s free cash flow is now projected to go “negative” in 2027 and 2028 due to the cash they’re pouring into the AI buildout.

Okay, let’s play this forward a bit.

Frontier AI models cost an insane amount of money to train (hence OpenAI, Anthropic, and xAI raising hundreds of billions of dollars to capture and/or maintain their leads). Data centers cost an insane amount of money to build. Private credit is a big source of financing for datacenter construction. Frontier AI models are (allegedly) killing a lot of SaaS companies with their expensive-but-ever-improving models. Private credit lent hundreds of billions of dollars to SaaS companies under the assumption that their EBITDA and revenue were, in fact, stable.

The existential risk facing the big AI companies is that either 1) they can’t secure financing to pay for GPUs or 2) they can’t secure the compute itself needed to train models. That compute constraint is alleviated through datacenter construction. Datacenter construction requires funding, and a big source of that lending is now coming under pressure as the market is stress testing the “value” of private credit funds’ books. Throw in a not-crazy possibility of an interest rate hike due to inflation (thank you, war in the Middle East!) that could further hinder refinancing opportunities on these struggling software loans, and, well, we’re in an interesting spot.

I’m not calling for the imminent collapse of the AI industrial complex, but it is more than ironic for me that AI seems, in 2026, to be primarily displacing 1) the very people who built it (software engineers) and 2) the very parties who are funding it (private credit).

Welcome Back, Trevor Milton

GOATed fraudster Trevor Milton parlayed his political pardon into a new gig as the CEO of Utah-based SyberJet Aircraft. If you don’t remember, Milton took his hydrogen-powered truck startup, Nikola, public through a SPAC in 2020. At one point, it was worth more than Ford despite never producing a functioning truck (though they had some sick rendered images!). It later turned out the the whole thing was a house of cards, with Hindenburg research publishing a scathing short report that, among other things, showed that video of the “battery-powered” truck was actually only gravity-powered: “live” footage was really just the truck rolling down the hill with the camera rotated.

Anyway, Milton went to prison for securities and wire fraud after, among other things, getting busted misleading investors, but then he was pardoned by Trump after, among other things, playing up “political victim” as much as possible and donating a few million to the Trump campaign. (This is a great move, by the way. Sam Bankman-Fried has been trying to tweet his way into a pardon for months).

And now Milton runs a plane manufacturer. Look, on one hand, I think it’s not great that someone who lied about a truck’s motor actually functioning is now running an aircraft manufacturer with the goal of creating “the first light jet to focus on artificial-intelligence flight” (like what does that even mean?) But also, I respect the balls it takes to lie your way to a $40 billion market capitalization for a vaporware truck company, so why not run it back? Would I ride in the plane? No. Would I buy the stock? If history is any indicator, probably.

Good Content:

Fun, nine-year-old piece from Byrne Hobart on how he accidentally became an entrepreneur before accidentally working for a hedge fund.

Wild deep dive piece claiming that SOC-2 compliance startup Delve has been running a fake business. A couple of thoughts: 1) if true, this validates my thesis that all of these “street interview” videos are a grift, and 2) Forbes 30 under 30 has another fallen angel.

Really fun interview with Travis Kalanick discussing his new company + thoughts from Uber on TBPN. This dude rocks.

Excellent conversation between Hubspot founder/Sequoia partner Brian Halligan and OpenDoor’s new CEO Kaz Nejatian.

Other Notes, Thoughts, Riffs:

Etiquette School in NYC: Last November, after noticing the disconnect between Silicon Valley’s venture-backed abundance of financial capital and lack of social etiquette, We (Slow Ventures) hosted an “Etiquette Finishing School,” (TechCrunch coverage here) in which we had three hours of panel discussions covering everything from how to dress to how to eat your caviar. The event was a real hit, so now we’re running it back next Tuesday in New York City! Signup link is here; we have a few slots left and we’re prioritizing RSVPs from NYC-based founders. If you’re around, sign up and come hang.

Creator AI bootcamp in SF: Another Slow Ventures plug: we’re also hosting a “Creator AI Bootcamp & Hackathon” in San Francisco next Thursday and Friday. For any creators (Youtubers, Substackers, whatever) reading this that have been wanting to up their artificial intelligence game, we’re hosting a two-day bootcamp teaching you everything from proper set up / tool usage to actual workflows for automating the boring stuff. If you’re interesting, RSVP here.

Ever since buying / building this bookshelf from Ikea a couple of months ago, my rate of purchasing physical books instead of Kindle has exploded. Highly recommend.

- Jack

I appreciate reader feedback, so if you enjoyed today’s piece, let me know with a like or comment at the bottom of this page!

The doom loop: Private credit was lent to SaaS vendors under the assumption of stable EBITDA. Now, those marks are impaired because AI has eliminated their pricing power. The buildout isn't the problem. The bet on SaaS stability was. Blue Owl backed the wrong layer of the stack.

Hey Jack, you wrote you weren't expecting a "Salesforce-level app" from vibe coding, but that's pretty much what I've ended up building.

In fact it's better, cuts out all the stuff that frustrated me about Salesforce over the years. It was not a push of a button thing, I've been at it for months, but the end result is really solid.

Check it out yourself at flowstack.6away.ai