What's a Reputation Worth?

Approximately $750M, apparently

Welcome to Young Money! If you’re new here, you can join the tens of thousands of subscribers receiving my essays each week by adding your email below.

A strong reputation often creates wealth.

Customers are more likely to purchase from companies they trust. Readers are more likely to read sources they trust. Investors are more likely to invest their money with asset managers they trust.

How do you build a strong reputation? By word of mouth.

Someone receives a recommendation from someone they trust, and they give it a try. If they enjoy said recommendation, the cycle repeats as this second person recommends this thing to someone else they know. Sooner or later, once one’s network of recommendations reaches a critical mass, a reputational flywheel takes shape.

And these flywheels can quickly turn exponential.

Millionaires tell their friends who their asset managers are, and those managers’ AUMs increase by a factor of 10. Multiple podcast hosts, mentors, and speakers around the world begin recommending the same book, and sales go through the roof. A few well-manicured lawns in a small town employ the same lawn care service, and suddenly everyone in that area code wants to be a customer. You get the idea.

Over time, your reputation is the sum of these collective recommendations.

A strong reputation is good for business because it represents a large and/or valuable customer base, but this symbiotic relationship between reputation and wealth develops slowly. Financially speaking, you can be an overnight success if you have some stock options that suddenly become quite valuable thanks to a timely acquisition, but there are no reputational shortcuts, because trust takes time.

Once you have built a strong reputation, you can leverage it to further increase your earnings.

Take The New York Times, for example. The Times has built a strong reputation as one of the go-to news sources in the United States, and it now boasts an audience of 9M+ readers. While the Times makes ~$1B from digital subscriptions each year, it also makes a healthy $523M from advertising revenue. The reason? It leverages its reputation as a publication to entice advertisers to pay for ad slots. Advertisers know the Times has a large, engaged audience (which was built over time as its reputation grew), and they are willing to pay hundreds of millions of dollars for exposure to that audience.

When done correctly, this advertising model benefits all three parties: The company or platform hosting the ads makes more money, the advertiser gets exposure to a larger, valuable audience, and the customer gets cheaper (or free) services than they otherwise would.

But the advertising model isn’t without risks. Poor advertising partners undermine the reputation of the platform or company running the ads, and a weakened reputation has negative consequences.

If a financial newsletter, podcast, or YouTube channel claims that a crypto product is a safe investment, for example, and three months later, it’s revealed to be a blatant scam that caused a not-insignificant portion of their audience to lose a lot of money, that creator/platform loses audience trust. If The New York Times were to primarily run political and otherwise low-quality ads, the publication would lose audience trust (see Twitter for an example of what happens when the quality of advertisers drops).

As trust erodes, readers and listeners are less likely to click further ads, and some may quit engaging with the content entirely. This, of course, is detrimental to the long-term health of the publication. It’s a short-term financial gain that hurts the long-term value of your platform.

Media publications aren’t the only parties that monetize their reputations. Asset managers who have years of strong performance and good relationships with their clients can more easily launch new funds. Founders with successful exits can more easily raise venture capital. The list goes on and on. But, as with advertising, reputation matters.

If you lose that reputation while chasing the next dollar, you might find it impossible to win back.

In 2020 and 2021, Chamath Palihapitiya was the brightest rising star in the investing world.

In 2019, the former Facebook exec-turned-venture capitalist took Richard Branson’s Virgin Galactic public through his first SPAC: Social Capital Hedosophia (ticker: IPOA). It seemed like an odd deal at the time, considering that 1) no one really knew what SPACs were and 2) Virgin Galactic was years from generating any real revenue, and the stock floundered for months.

But then Covid happened. And quantitative easing kicked into high gear. And suddenly, with interest rates at historic lows, pre-revenue companies valued at billions of dollars didn’t seem quite so far-fetched, and SPACs became the hottest commodities on Wall Street as they gave investors an expedited method for taking otherwise financially questionable companies public quickly.

Intentional or not, Chamath had kickstarted a wave of hundreds of SPACs that would hit the market over the next three years. And he capitalized on the momentum. Virgin Galactic’s stock skyrocketed in early 2020, so Palihapitiya doubled down by launching 9 more SPACs, and he made sure to talk his book.

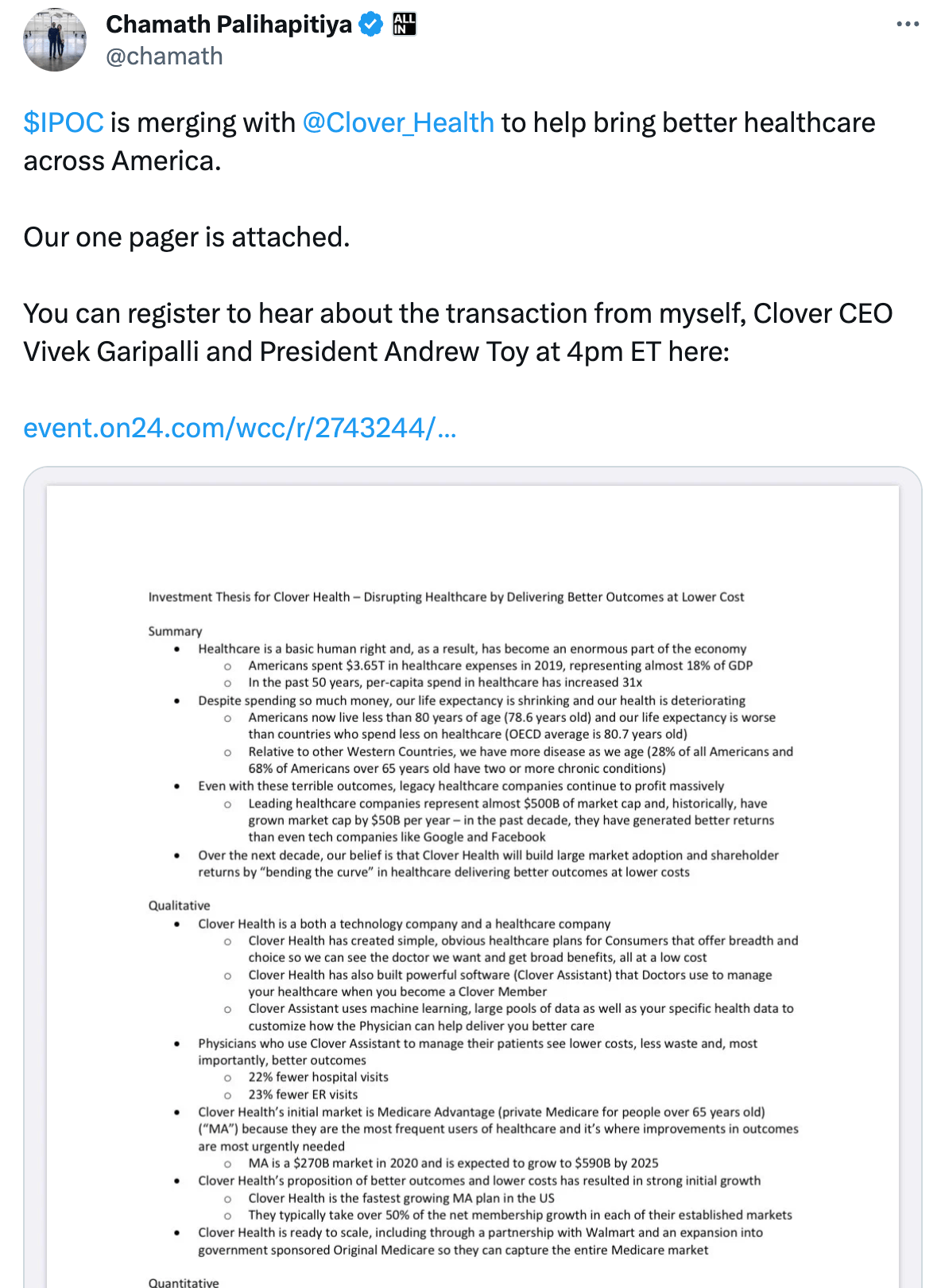

Chamath was very active on Twitter, and he painted himself as the billionaire on the Little Guy’s side, the man democratizing access to financial markets by giving retail investors access to these SPAC deals (deals that, if closed, he would stand to make millions from, regardless of stock performance), so they could invest in “disruptive” companies pre-IPO. And anytime one of his SPACs signed a binding merger deal, he tweeted out a one-pager investment thesis to his 1.3M followers. These followers rewarded his generosity by running the stock’s price up 50, 100, and 200%

During the GameStop short squeeze, Palihapitiya repeatedly attacked Robinhood for unethically selling payment for order flow to HFT firms like Citadel, and he encouraged his followers to switch over to SoFi, which had conveniently gone public through a merger with one of his SPACs (and which also happened to sell order flow to HFT firms like Citadel, though he forgot to mention that part).

But you know what? His strategy was working. While SPACs as a whole were a mixed bag, Chamath’s SPACs were outperforming the broader market through the first half of 2021.

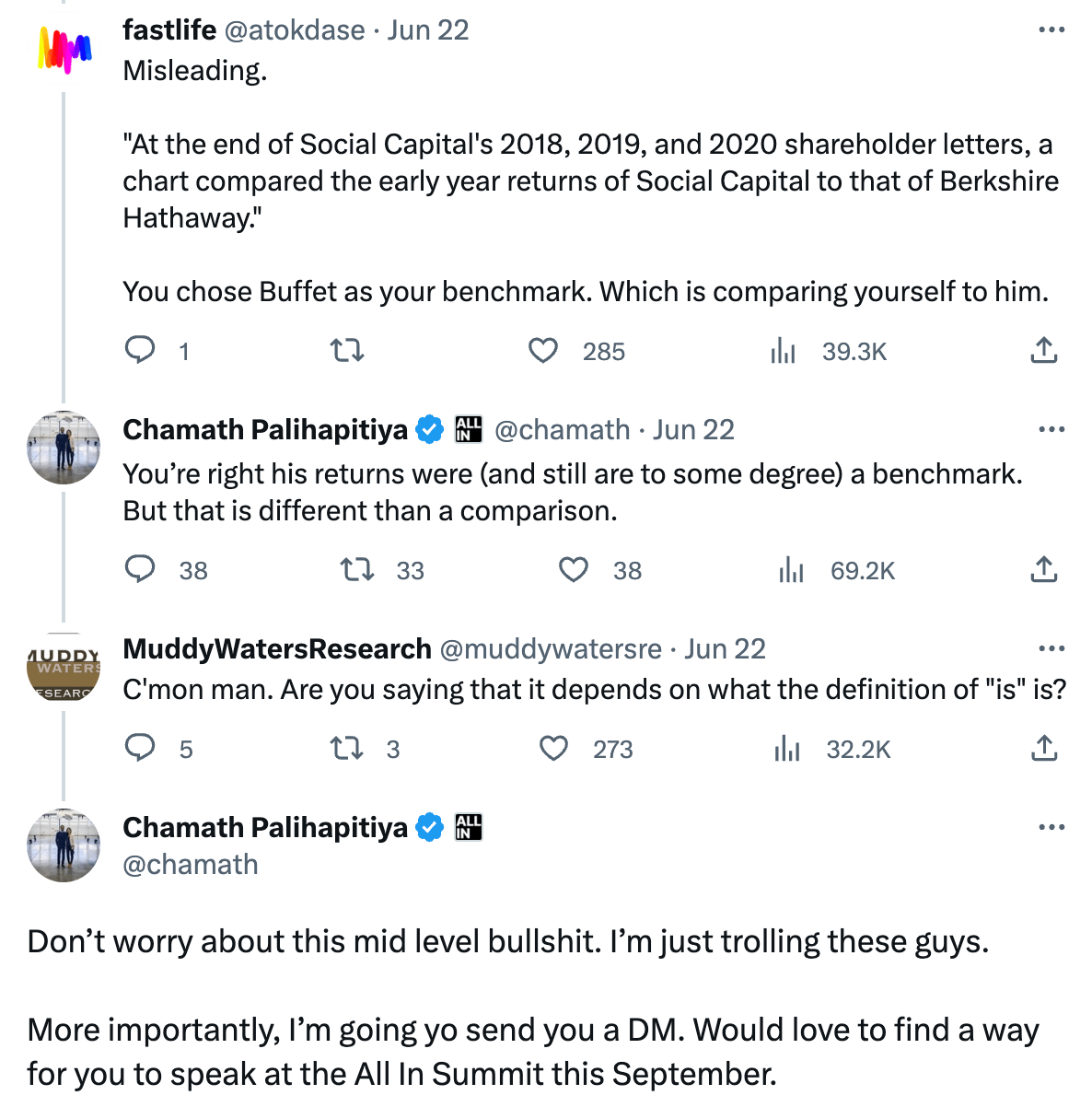

Comparisons to legendary investor Warren Buffett were made by both Chamath and others (in fact, he used Berkshire as a benchmark in his own 2020 annual report), and he claimed that the only reason he would sell any shares was to release cash for other endeavors.

But cracks began to show in December 2020, when, despite his outspoken bullishness on the company, Chamath sold 3.8M Virgin Galactic shares to “manage his liquidity,” before selling the rest of his personal stake (though he did retain other shares through his investing firm, Social Capital) two months later.

And then, after peaking in February 2021, the SPAC market collapsed. The Fed began raising rates, companies that went public in 2020 started missing their optimistic financial forecasts, and investors chose to move their money elsewhere.

Rocket emojis and “one-pager” word docs no longer supported billion-dollar valuations, and Chamath eventually wound down his last two remaining SPACs to return cash to shareholders.

Despite the post-QE hangover that decimated the more speculative corners of equity markets, Chamath did alright, pocketing a $750M profit from the SPAC trade when it was all said and done. It turns out that when you sponsor a series of deals structured in a “Heads I win, tails you lose,” fashion, it doesn’t really matter if the deals are trash.

Just promote the hell out of the stocks, liquidate once the deals close, and let someone else hold the bag.

If this was purely a money game, a means to a financial end, it wouldn’t really matter. Did Chamath break any laws? Not that I know of. If anything, he just took advantage of regulatory oversights. And if his Twitter followers were willing to buy what he was selling? Who cares. Take your $750M, go ghost, delete Twitter, and move to a private island.

But Chamath isn’t just playing a money game.

Ryan Holiday once said that everyone wants to be rich, but the rich just want to write books. Chamath was a multi-billionaire before the whole SPAC thing, and his ambitions had long since moved beyond a larger net worth. Chamath flirted with running for governor of California, he tweets his thoughts on economic and financial topics almost daily, and he is dedicated to his All-In podcast.

He’s playing the status, respect, and thought leadership game. And he’s losing that game because of his involvement in the SPAC market.

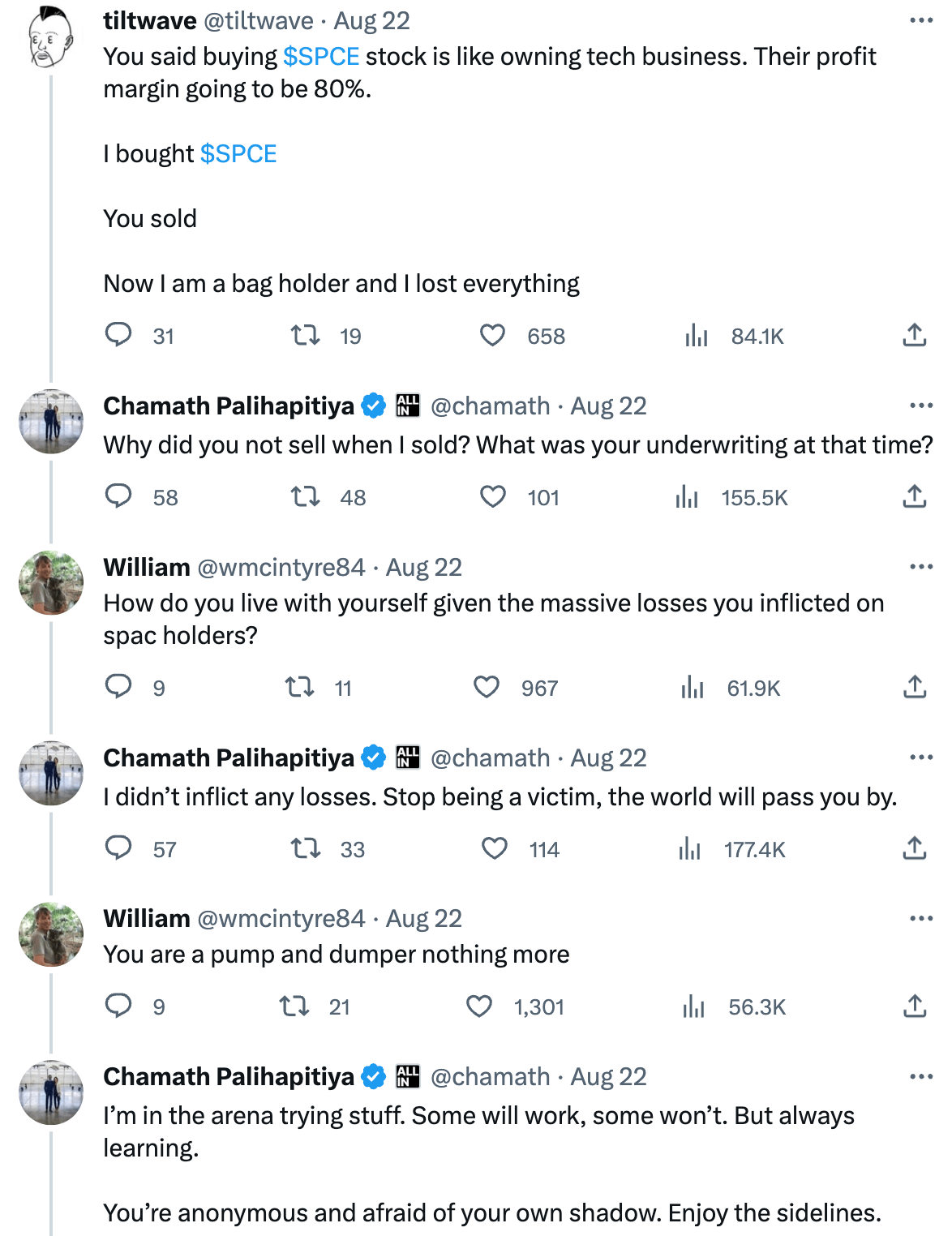

Twitter is a fascinating site because it provides a level playing field for anyone and everyone, regardless of net worth, to interact as equals, and over the last few weeks, Chamath couldn’t help but snap back at each and every critic…

… and attempt to play revisionist history, downplaying his own comparisons to Warren Buffett and his responsibility for shilling different SPACs on his following.

Anything to save face. But it isn’t working.

That $750M wasn’t free: the cost was his reputation. And he just can’t get over it. Why not just say, “You’re right! I did call myself the next Buffett! I did take some questionable companies public! And guess what? I made bank doing it!”

Because it isn’t about the money. It’s about his image. Respect. But you can’t just buy a new reputation once it’s tarnished.

Was the money worth it? I have no idea. Would I trade my reputation for $750M right now? Who knows? But if I were richer than God, I hope that I wouldn’t trade something priceless for a few more dollars.

Reputation can be leveraged for wealth, but it’s a risky trade-off. The speed at which one’s reputation can be converted to dollars is highly correlated with the risk that those dollars will also destroy one’s reputation.

- Jack

I appreciate reader feedback, so if you enjoyed today’s piece, let me know with a like or comment at the bottom of this page!

Young Money is now an ad-free, reader-supported publication. This structure has created a better experience for both the reader and the writer, and it allows me to focus on producing good work instead of managing ad placements. In addition to helping support my newsletter, paid subscribers get access to additional content, including Q&As, book reviews, and more. If you’re a long-time reader who would like to further support Young Money, you can do so by clicking below. Thanks!