Trickle-Down Euphoria

Line goes up, until it doesn't.

Welcome to Young Money! If you’re new here, you can join the tens of thousands of subscribers receiving my essays each week by adding your email below.

Public Market Euphoria

2020 was an interesting year in the stock market. The fastest decline in history was immediately followed by the fastest recovery to all-time highs in history, and every single growth stock was a rocket ship. By early 2021, some tech stocks were trading at 100x revenues, and investors didn't bat an eye. No price is too high for a company growing sales 300% year over year, after all.

Ark's CEO Cathie Wood was the hottest name on Wall Street, as her bets on "disruptive growth" had turned Ark's flagship ETF into one of the best performing funds on the market.

By traditional metrics, most growth stocks were grossly over-valued. Plenty of companies were trading at 50x sales, when price to sales wasn't even a conventional measurement just two years earlier. But in a low interest rate environment where companies are growing at blistering paces, these high valuations had become the new norm.

When one stock is trading at 50x sales, it's overpriced. When every stock is trading at 50x sales, that becomes the benchmark (at least in the short-term). It's fascinating how quickly we normalize outliers.

So tech companies are worth $10B+ on $200M in revenue. Investors and employees with stock options are making millions thanks to the market's new-found love for tech.

One group of people was stuck outside the party looking in, and they desperately wanted an invite. This group? Late stage private companies.

Initial Public Offerings

Imagine that you are a late stage private company, and you see the stock prices of public tech companies / Covid-beneficiaries like Zoom and Peloton doubling, tripling, and quadrupling. Employees are printing money from their stock options, while your private shares are illiquid.

If you are an investor or employee with stock options, you obviously want to reap the benefits of favorable market conditions, and your company probably just had one of its best quarters in its history.

So you put together a pitch deck highlighting your insane 200% year over year revenue growth. You hire Goldman/Morgan Stanley/some other fancy bank to help with the IPO process. You craft an enticing narrative, telling investors that favorable tailwinds provide a massive runway for future growth. That 200% growth last quarter? That's just the beginning.

Now obviously that 200% growth won't be sustainable; demand was merely pulled forward. 2021 was a one-off acceleration for most companies, and 2022 will be a different story.

But if you can execute your IPO quickly enough, the inevitable growth slowdown won't be visible until after your 180 day lockup expires. If you can sell your shares at peak valuations, who cares if the stock crashes six months later? You cashed out, homie.

And guess what? 2021 had a lot of IPOs.

Logan Bartlett is an MD at Redpoint Ventures (as well as an avid tweeter and podcaster), and he posted a great thread last month highlighting the state of private markets. I'll reference the below Twitter thread from Logan a couple of times here.

$681B in IPOs in 2021 alone. Companies definitely took advantage of the opportunity presented by public markets.

Follow the Leader

Public market euphoria created IPO euphoria as private investors rushed to cash in when their companies approached nosebleed valuations. Eventually, this euphoria found its way to private market funding rounds too.

Private markets are often lagging indicators of public markets, given their illiquidity and infrequent funding rounds. Additionally, valuations in private markets are often marked against public companies. Public SaaS companies are trading at 50x sales? Private companies will look to raise funding at 50x sales.

Another tweet from Logan highlighting the uptick in VC funding last year:

While the number of deals closed in 2021 was up just 27% from 2020, the amount of capital invested increased by 98% year over year. How did this happen? Investors were throwing a lot more money into individual start ups, giving companies notably higher valuations than in years past.

The reason was simple: private companies looked at public companies trading at ~50x sales and said, "We should also be trading at 50x sales." Investors looked at the same public companies and thought, "The market is supporting 50x sales." So they agreed to invest at 50x sales.

Remember, if one company is trading at 50x sales, it's expensive. If every company is trading at 50x sales, it's the benchmark.

No one stopped to think that perhaps everyone was overpaying for everything, every "growth" company was now priced for perfection, and any slowdown in growth could make the whole thing collapse like a house of cards.

What Happens When the Music Stops?

The problem was that investors mistakenly believed this accelerated revenue was a permanent shift in growth trajectory, while Covid had actually just pulled forward their existing trajectories. 300% growth is phenomenal, but it's not sustainable.

When the music was playing, we had to dance. And for more than a year, we danced indeed. But as the world adjusted to remote and tech-heavy work, the future growth for these companies slowed, and this deceleration showed up in earnest in Q1 2022.

200% revenue gains from 2020 to 2021 became 20% gains from 2021 to 2022. Publicly companies that were trading at 40x sales were cut in half instantly, and the clock was ticking on private markets.

Those companies that went public at peak 2021 valuations? Let's check on them now.

I'm going to share six stock charts with you guys: Affirm, Robinhood, Coinbase, DoorDash, SentinelOne, and Duolingo.

What do a BNPL financer, stock exchange, crypto exchange, food delivery service, cybersecurity provider, and foreign language educator program have in common?

They all went public in the last year or so

They've all gotten wrecked over the last eight months

Again, management likely knew that 200% growth wouldn't last forever, and neither would these nosebleed valuations. But if you have illiquid shares, and the market is paying top dollar for high-growth tech, why wouldn't go you public right now?

Over the last decade, companies have stayed private for longer and longer, leading to most of the gains happening in private markets. 2021 was the perfect final act for this decade's private market investing, as investors and employees were able to top tick their public listings.

IPOs in 2021 weren't an opportunity for public market investors to invest in fast-growing, innovative companies. IPOs were liquidity events that let early investors secure the bag, while new investors were left holding it.

Robinhood democratized finance by bringing IPO allocations to retail investors. A process typically reserved for institutional investors, finally the little guy could get shares before they debuted on the public markets. However, Robinhood made sure to tell investors not to sell their allocated shares on Day 1, or they might be penalized for "flipping" shares.

Here's Why You Can't Sell Your Robinhood IPO Shares On The Platform Yet

While this message is common across most brokerages, it is interesting that Robinhood specifically warned investors about flipping shares of Robinhood itself, while the company's CEO dumped $45M worth of stock the first day it was publicly traded. Everyone needs to HODL, except the CEO of the company I suppose.

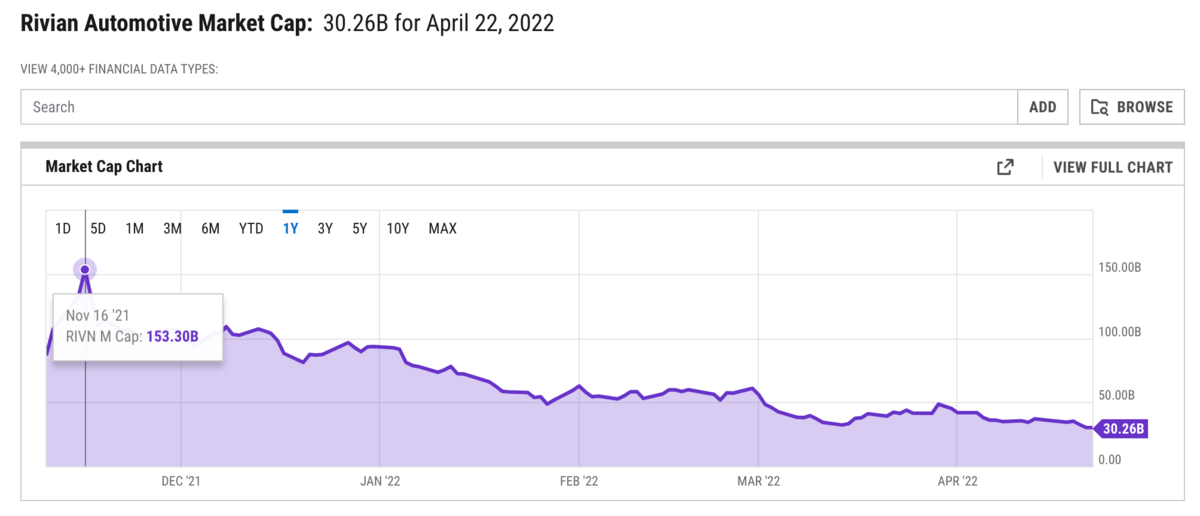

Meanwhile, an EV truck manufacturer that had sold zero vehicles hit a $153B valuation on its first few days of trading. 50x price to sales is expensive, but if you have no sales whatsoever, your valuation can be whatever you want.

While Robinhood and Rivian both performed well in the days following their IPOs, they have since fallen back to earth with the rest of publicly traded growth stocks. Private market prices, however, have remained elevated. One fund manager believed this created an enormous arbitrage opportunity for public companies:

But the reality was that private markets lag public markets, not vice versa. This wasn't an opportunity for public stocks to regain their nose-bleed valuations. It was the calm before the storm of private market mark downs.

And when these markdowns started, there was no stopping them.

We have watched this play out in real time in 2022.

Tiger Global, the world's best performing hedge fund of the last decade, suffered a 34% drawdown in Q1 of 2022 alone. Instacart marked down its own valuation by 40% in March. A 1-click checkout company, Fast, shut down just one year after raising $100M, and the company only managed $600k in revenue in 2021.

When mean reversion hits, it hits. So how do these euphoric valuations happen?

We all claim to be long-term investors, but 12 months can normalize outlandish prices for many. Everyone is chasing outperformance, and for a year or so, no price was too high for growth and innovation. High-valued public companies pushed late stage private companies to pursue high-priced IPOs. High-priced IPOs pushed other private companies to raise funding at the highest valuations possible.

When the whole market is overvalued, expensive companies look fairly priced compared to each other. The problem is that when valuations come back to reality, everything gets pulled down equally.

At the end of the day, entry points will always matter. Trillion dollar addressable markets, groundbreaking technology, and phenomenal forecasts mean nothing if you are paying $10B for a company making $100M in revenue.

It's not just what you buy that matters, but how much you pay for it.

Happy Monday, let's go YOLO some billion-dollar, zero-revenue growth stocks.

- Jack

I appreciate reader feedback, so if you enjoyed today’s piece, let me know with a like or comment at the bottom of this page!

Young Money is now an ad-free, reader-supported publication. This structure has created a better experience for both the reader and the writer, and it allows me to focus on producing good work instead of managing ad placements. In addition to helping support my newsletter, paid subscribers get access to additional content, including Q&As, book reviews, and more. If you’re a long-time reader who would like to further support Young Money, you can do so by clicking below. Thanks!