Software is Dead, Long Live Software

Some thoughts on the "AI kills software narrative" post-Figma earnings.

Welcome to Young Money! If you’re new here, you can join the tens of thousands of subscribers receiving my essays each week by adding your email here. And if you like my blog, you should pre-order my first book, Young Money, by clicking below:

Today’s letter covers my thoughts on broader investor FOMO into semiconductor and memory stocks, why software might not be dead, and some nuance on how AI could make certain software players even more valuable.

SaasPocalypse: Q1 2026

Claude Code got really good around Thanksgiving of 2025 when Anthropic dropped Opus 4.5. If you used AI coding assistants in June 2025, you probably found them to be “useful but messed up a lot,” requiring way too much handholding to be left alone, lest they destroy your codebase while unsupervised.

That changed with Opus 4.5 (and, soon thereafter, similar updates to OpenAI’s models), and after every developer and their mom played with these coding assistants over the holidays, consensus quickly became, “Software is cooked, Claude Code is GOATed.”

The result: investors began dumping software stocks hand over fist, with the iShares Tech Software ETF down ~37% in Q1 of 2026.

Memory Stocks to the Moon

This selloff was amplified by the fact that, at the same time, everyone began piling money into semiconductor and memory stocks like Intel, SK Hynix, and Micron, as investors who had previously balked at AI thought, “Maybe AI isn’t a bubble, and maybe I’m underexposed.”

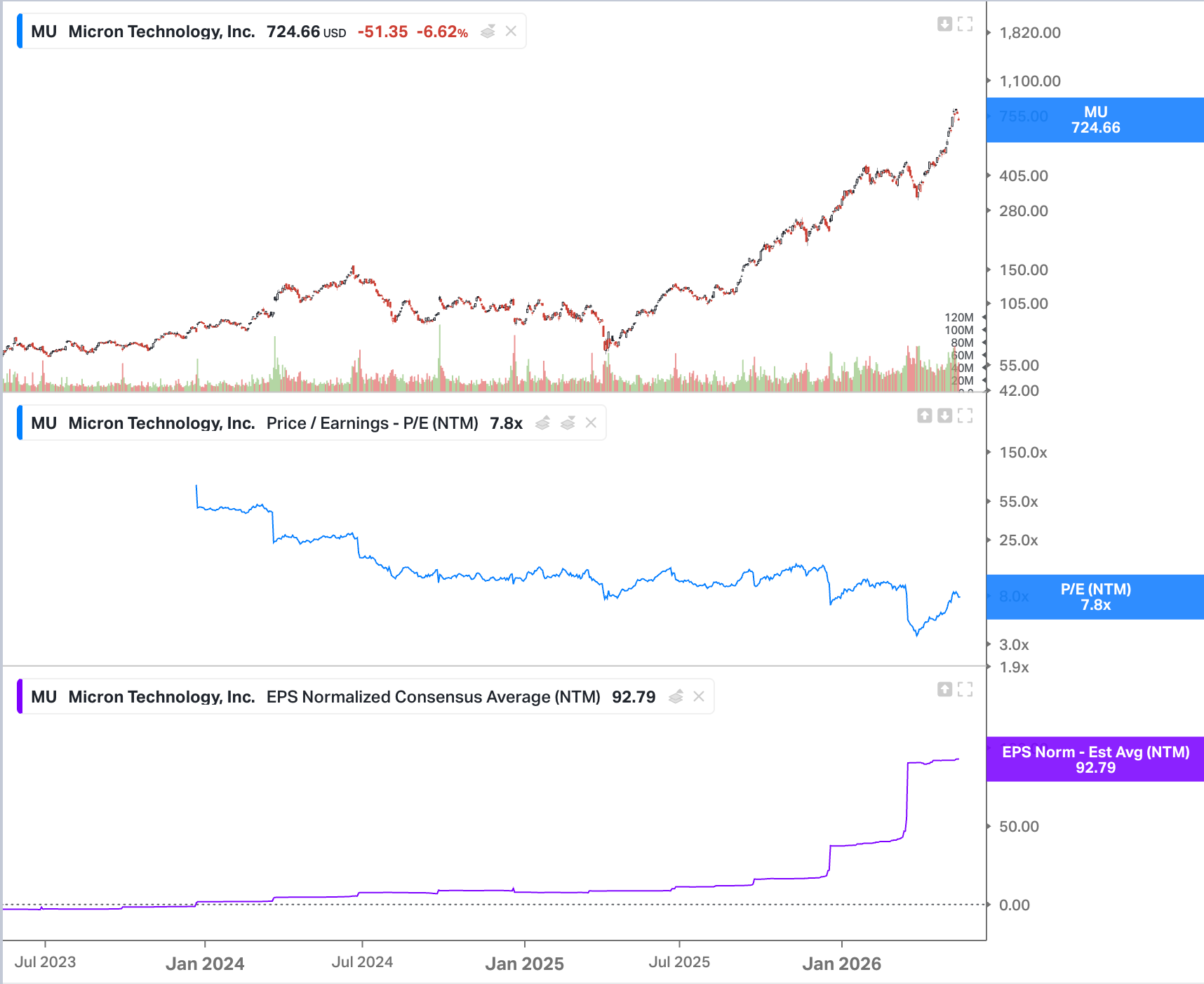

The irony is that, despite several of these stocks running up 1000% or more in the last year, they’ve actually gotten “cheaper” on a P/E basis.

Micron’s stock has 10x’d since April 2025, but it’s actually cheaper on a forward earnings basis than it was a year ago as demand for memory thanks to the AI buildout is just insanely high, so memory providers are printing money hand over fist.

Micron’s net income in 2024 was $1.4B. In 2025 it was $9.5B. The company is projecting $68B in profit in 2026, and $112B in profit in 2027. Free cash flow is jumping from $121M in 2024 to $36B in 2026. Memory is historically a low margin, cyclical business, with Micron’s gross margins climbing from 20% in 2016 to 59% in 2018, before collapsing back to 31% in 2020. They were 41% in 2025 and they’re projecting 77% and 79% in 2026 and 2027, respectively. It’s not a “bubble,” the AI bottleneck companies are just making an insane amount of money now.

And, if you are a fund manager, there is a very real “career risk” in missing the AI infrastructure wave. The S&P and Nasdaq are RIPPING given that they’re so overweight semiconductors right now, so if you’re underperforming your benchmark AND you missed the thing powering the indices, you risk having your LPs pull out their capital and allocating elsewhere.

So, now that these stocks have melted up, and may very well be poised to keep melting up, many funds are dumping their other positions to allocate toward semiconductors accordingly. The result? Even more selling of software stocks.

It’s a vicious feedback loop: the AI infrastructure trade maintains momentum, forcing more investors to pile in or risk missing out, leading to more selling behavior is the software sector, adding more fuel to the “software is dead” narrative (as price often drives narrative), causing more people to sell software to buy AI stocks, and... you get the idea.

Combine that with the fact that so much of the market is either index funds, retail investors chasing momentum, or multi-manager hedge funds playing quarterly earnings rather than taking 12-18 month perspectives, and you just don’t have a lot of buyers for software stocks right now.

Where Does Software Go From Here?

To be clear: AI is very much a threat to software. Nontechnical folks can build functional code in minutes. Technical folks can deploy dozens of AI agents to crank through tasks for them simultaneously. Companies are reimagining their internal workflow processes around AI at the same time that newer, leaner, faster startups are competing with their more mature competitors for customers, cutting into incumbents’ pricing power. Some software companies, particularly those that have historically provided “personal productivity tools,” are likely cooked, or, at least, face an uphill battle.

But also, while “software” is a sector, not all software companies are created equal, and we’ve started to see a dispersion in outcomes for different software companies’ stocks. For example, Palo Alto Networks sold off hard in Q1 with the rest of software, until, wait! It turns out that AI opens a whole swarm of security vulnerabilities, which could be quite bullish for a cybersecurity stock.

I think we’ll continue to see a greater and greater bifurcation in software names as the overarching narrative of “AI is going to kill all SaaS” is disproven by specific companies putting up stellar earnings, and, at some point, the market will begin to respect that resilience as proof that maybe AI won’t kill “everything.”

Though, personal productivity tools like Asana are probably cooked.

Another recent example: Figma. I bought some Figma stock a couple of weeks ago largely because the stock’s price action just felt totally detached from reality. As a reminder: Figma is a collaborative design platform that went public last summer, briefly hitting $142 per share in August. Its stock price has since collapsed to ~$17 per share as of May 2026.

Figma was, at its IPO, overvalued. It was briefly worth ~$56 billion post-IPO, or 40x 2026 revenue. Those multiples don’t work any more in 2026.

(Also, an aside, but Figma was one of the best private software companies, and it got smoked in the public markets. There’s plenty of overvalued private companies waiting to get cut in half in the public markets, in my humble opinion).

The stock then collapsed by ~85%, thanks to a combination of “this stock is overpriced,” the broader narrative of “SaaS is cooked,” and Anthropic launching its “Claude Design” tool (which is wonderful; I’ve used it to build some social media templates for my book promotions).

At a $9B market cap and ~7x sales, it wasn’t “cheap,” but if you take the view that 1) this company is growing fast and will continue to do so, 2) is spitting off high margin free cash flow (a rarity for SaaS businesses these days), 3) could very well benefit from the AI boom, and 4) is led by an AI-pilled founder who still very much wants to win, then, well, while the broader narrative still sucks, the stock starts to look interesting.

And, while the “AI will kill software” has some truth to it, I think the more nuanced reality is that AI changes which software is more valuable. At my job, for example, we’ve rearranged some of our internal software tooling, but I’m actually using Notion more now as a dashboard / interface layer for tracking our dealflow and pipeline. We’ve rearranged a lot of the under the hood flows, but Notion as a collaborative dashboard tool has actually become more valuable, not less. My high-level take is that a lot of software companies that serve as coordination layers of multiple parties’ information may benefit from AI, particularly as more and more agents take on larger and larger workloads.

So, I bought some Figma.

Their earnings came out last week, and the results were great:

46% YoY revenue growth (accelerating), 139% net dollar retention (highest in two years), 27% adjusted FCF margins, etc. There’s still some flags (gross margin pressure as AI inference is more expensive than normal software margins, threats from Google / Anthropic, etc), but at least for now, the company is far from “dead,” and the stock ended the day up 13%.

Anyway, I think we’ll see a select group of software names start to prove that “AI just might not kill me,” which, of course, will be ironic as so much money is right now pivoting to the memory names that are up 1000% in the last year.

Happy Monday, let’s have a great week.

- Jack

I appreciate reader feedback, so if you enjoyed today’s piece, let me know with a like or comment at the bottom of this page! And make sure to pre-order my first book, Young Money, by clicking below:

Other Notes, Thoughts, Riffs:

Another shameless plug to follow my new Instagram as I ramp up this book marketing campaign.

Claude Design is seriously fantastic for creating marketing materials and content. I used it last week to make some templates for book promo stuff on social media, and I’ve been loving it. (see examples below). If you have a Claude account, you should check it out.

People are starting to learn that not all SaaS companies are the same, but it's taken those people too long to realise that. It's more nuanced than the current narrative that everyone seems to be running with and taking at face value.

The dispersion in SaaS (which I've spoke on in various writings) will be important going forward. From a PE/PC viewpoint, some companies are vertical SaaS that have deep workflow integration, sticky enterprise contracts & limited AI substitution risk. These types may be able to refinance or A&E through the maturity wall and possibly come out of it relatively unscathed. For companies closer to Medallia, A&E isn’t an option for horizontal SaaS businesses with generic problems LLMs can solve, as they lack the terminal value.

There’s always nuance behind the “x sector is cooked” narrative. Some of it is finding the leader or best in the field and assessing their ability to adapt. It doesn’t always work (Chegg is a good example of when it doesn’t) but there are gems to be found when broad sentiment looks the other way.