$660M in a Day: The Big Oil Short

What happened the day the oil market broke

Welcome to Young Money! If you’re new here, you can join the tens of thousands of subscribers receiving my essays each week by adding your email below.

The last few years in financial markets have been anything but normal. GameStop hit $400 a share (pre-split). Nikola Motors was briefly worth more than Ford. NFTs were worth millions.

But the most insane market moment in the pandemic era wasn't a meme stock, cryptocurrency, or SPAC. It was sweet, sweet crude oil.

Before GameStop started, DogeCoin barked, and Trump tried to make SPACs great again, the oil market experienced the unthinkable:

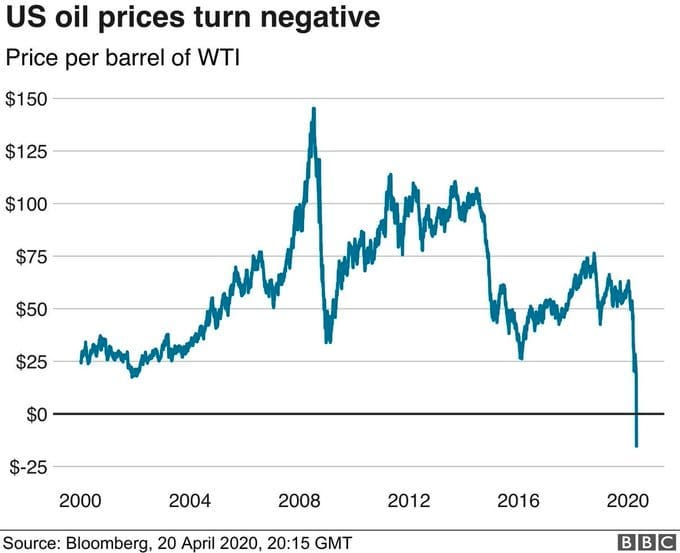

On April 20th, 2020, oil hit -$40 per barrel.

Today, oil costs ~$90 per barrel. Two years ago, you could get paid ~$40 to take delivery of this same asset.

Oil had never turned negative before and will likely never go negative again. Truly a "once-in-a-lifetime" occurrence. But these rare occurrences also create once-in-a-lifetime opportunities.

This is the story of fortunes won and lost the day the oil market broke.

*Broader sources for this piece are linked at the bottom. Specific data points are linked throughout.

On April 20th, 2020 in Essex, England, Paul "Cuddles" Commins prepared for another day in the markets.

Cuddles was a veteran commodities trader who earned his stripes (and affectionate nickname) in the pits of London's International Petroleum Exchange. The IPE trading pit in the 80s and 90s was like a Wild, Wild West where The Wolf of Wall Street met Peaky Blinders.

As algorithmic and high-frequency trading went mainstream, Cuddles started his own operation, Vega Capital, in Essex with eight other traders.

The nine members of Vega Capital, some of whom were sons of Commins' friends, legally operated as independent traders, but they often worked together. Outside of work, they could be found deleting pints of beer while watching their football club, West Ham United.

April 20th was gearing up to be a busy trading day for the lads in Essex. It was the last trading day for the May WTI Crude Oil futures, and the CME had warned that oil could hit zero, or even turn negative, as May contracts approached expiration.

How did we get here?

Let's back up two months.

In February of 2020, college students were planning spring break trips, millions of workers were commuting to and from the office five days per week, March Madness was around the corner, and the Chiefs had just won the Super Bowl.

But a lot can change in two months.

In March, air travel screeched to a halt, college students were sent home from their universities, and white-collar employees around the world ditched their cubicles for home offices. No sports, no concerts, no live events whatsoever. Cities became ghost towns, resembling New York City in I Am Legend.

With air travel and work commuting now paused indefinitely, oil demand plunged, sending prices to levels not seen since 1998. To make matters worse, OPEC negotiations collapsed on March 6th, when Saudi Arabia shocked the world by increasing production and slashing prices despite the lowest oil demand in decades.

Global oil storage capacity shrank as demand fell because oil investors chose to temporarily store cheap oil with the intention of selling it on the market once prices recovered.

Collapsing demand, increasing supply, and minimal storage capacity created a perfect storm for the oil market to implode, but to understand why the market finally broke, we need to travel to the heartland of the United States: Cushing, Oklahoma.

Commodities such as oil trade on futures markets. There are multiple oil futures contracts (with each contract representing 1,000 barrels of oil), and the most common derivative is West Texas Intermediate (WTI) Crude.

Some oil contracts, such as Brent Crude, which is based on oil from Europe's North Sea, can be cash-settled at expiration, meaning that the oil itself doesn't have to change hands. Buyers and sellers of contracts can simply exchange the cash equivalent of the asset at its closing price.

WTI contracts don't allow for cash settlement, and anyone holding an expiring WTI contract must take delivery of 1,000 barrels of crude. But you can't simply fill a swimming pool with black gold, you have to take delivery in Cushing, Oklahoma. Cushing is a landlocked oil hotspot in the central US, filled with pipelines and storage tanks.

Because of forced delivery on contracts held through expiration, most traders would simply close their WTI positions before the contracts expired. The only parties interested in taking delivery were energy companies and similar operators.

When the oil market is functioning properly, buyers simply take delivery via pipelines, storage units, and fuel trucks.

But this oil market wasn't functioning properly.

Given the collapse in prices, it was becoming more profitable to pay for oil storage than sell the oil right away. And because Cushing was landlocked, and investors were renting up all available storage space, it was going to be difficult for any buyers to take delivery of the commodity.

On April 20th, with just one day until expiration for the May WTI futures, storage capacity in Cushing was approaching zero.

Back to our British traders.

When the futures markets reopened the evening before, May WTI contracts started trading at $17.63. However, the price dropped over the course of the session, falling to ~$10 per share by noon EST on the 20th.

Believing that the market weakness would continue, Cuddles and his team decided to short the expiring contracts. To avoid any delivery risk, they used something called a "Trading at Settlement", or TAS contract.

I don't want to bore you with the specifics of derivatives contracts, but basically, TAS contracts allow you to buy/sell futures contracts within five ticks of the contract's settlement price that day.

An example:

If WTI is at $20 and you think it will drop over the course of the day, you would "sell" the WTI futures for $20 per barrel while simultaneously buying the same number of TAS contracts. If WTI falls to $10, you lock in a $10 profit (really $10,000, because each contract represents 1,000 barrels) per contract, as you sold at $20, and profited from the $10 decline because you "bought back" your contracts at $10.

By buying and selling the same number of contracts, you have no obligation to take/provide delivery of oil. The contracts cancel out, and you make and lose money based on the price movement. The inverse is also true: you can buy WTI contracts and sell TAS contracts to bet on positive price movement.

Clear enough? Cool.

Our British lads had an appetite for risk this particular day, and they believed that oil would keep falling. So they shorted the WTI futures around $10 per contract, and they planned to cover their shorts at the end of the day with TAS contracts.

The Brits sold batches of WTI contracts, offsetting them with TAS purchases. For the next hour or so, prices were stagnant. The traders grew nervous, as they knew the market would become more volatile as it moved closer to 2:30 PM (when trading ends and settlement prices are calculated).

If a spike of buy orders hit in the afternoon, their short bets could quickly go underwater, costing them millions.

Then it happened.

Two hours until closing time an activity spike hit, but it wasn't buy orders. Traders began liquidating everything.

Why?

Because there was no storage in Cushing, the contracts had no buyers. No one could take delivery of the oil, so the WTI contracts became a game of hot potato where no one wanted to be left holding the bag when the clock hit 0.

Prices went into free fall as sellers panicked. No one wanted to be stuck with the expiring contracts. WTI prices fell to $5, then $0. With 20 minutes of trading left, the unthinkable happened.

Oil turned negative for the first time ever.

As for Cuddles and his team? They smelled blood and went in for the kill.

Per The Guardian, text records show that they doubled and tripled down on their short bet as prices went negative.

Please read these texts in a British accent:

“We pushed each other so hard for years for this one moment … And we f*cking blitzed it boys,” read one message. “Just keep selling it every 5 points,” another said. “You’ve just got to keep selling,” said another. “Everyone is going to be short and have ammo,” read another. “F*cking mental. I wanna see negative WTI prices,” read another.

Their ballsy bet paid off. The settlement price at the end of the day?

-$37.63.

So how much money did they make? Let's do some math. When you short WTI contracts and buy TAS contracts, you "buy" back your contracts at the settlement price.

So if you sell at $10, and buy back at -$37.63, you make $47.63 x 1,000 barrels, or a $47,630 profit per contract.

And the lads from Essex sold a lot of contracts.

Their final one-day profit?

Approximately $660M.

$73M per trader, give or take a few million.

So what do you do after netting $100M in a day? Whatever the hell you want.

One trader, Harry Lunn, founded an international polo team that competes in Argentina. Another, Elliott Pickering, created his own racing company, where he now spends his time driving Ferraris. Aristos Demetriou purchased a mansion and several $200,000 cars.

Of course, every trade has a counter-party. And a trade that nets $660M in a day? Well... someone had to take an L. In this case, several someones.

We all know that 2020 brought a wave of inexperienced traders to the stock and crypto markets, but the volatile oil markets enticed many to try their hand in commodities as well. Leverage makes commodities a dangerous game for new traders: one bad bet could leave you owing far more money than you initially invested.

While the CME issued a warning on April 15th that May WTI prices could go negative near expiration, some retail-friendly brokers, such as Interactive Brokers, failed to prepare for this scenario.

When oil prices fell below $0, Interactive Brokers still displayed "$0.01" per barrel, prompting many small-time traders, such as Syed Shah, to think the bottom was in. The 30-year-old Shah, who had $77,000 in his account when the day began, was shocked to receive a notice that he owed the firm $9 million.

Luckily, Interactive Brokers bailed out these traders to the tune of a $104M write-off for the brokerage.

But it wasn't just retail traders who made ill-advised bets. The Bank of China was the oil crash's biggest loser.

In 2018, the Bank of China launched an investment product called "Crude Oil Treasure" (COT) to provide individual customers with trading services tied to overseas oil futures.

The BOC certainly knew who they were targeting, with early advertisements saying things like, "Is there a profitable but interesting product for a new investor without any financial knowledge? Absolutely! That is Crude Oil Treasure!”

They also conveniently overlooked any risk disclosures, assuring investors that "Whether the price of crude oil rises or falls, it always can make money."

But there are no guaranteed returns in finance. COT was structured so that investors couldn't lose more than their initial investment as long as prices stayed above zero.

The Bank of China ignored the CME's warnings in the week before the crash, doing little to prepare for the possibility that oil could in fact go negative. On April 20th, believing that negative prices posed zero risk, Bank of China traders took the opposite side of Paul Commins's trade, buying WTI futures and selling the TAS contracts.

The $660M profit for Cuddles and company? It has nothing on Bank of China's $1.4B loss. But liability for the losses didn't fall on the bank, it fell on the retail investors.

Thousands of investors who believed their money was secure found themselves owing the bank twice as much as they had initially invested.

A month later, the Bank of China offered to shoulder the losses from negative oil prices, but they would only compensate up to 20% of investors' original investment.

Consider me shocked, and I mean shocked, that a product marketed as, "A profitable but interesting product for a new investor without any financial knowledge" imploded.

The final tally, assuming the Bank of China settled with all investors? $1.84B.

Down bad.

April 20th was a prime example of how fear, greed, luck, and skill have outsized impacts on markets. The only difference between making $660M and losing $1.84B is that one group bet on the impossible, and the other group believed the impossible could never happen.

Fortune may favor the bold, but markets punish the ignorant.

Happy Monday, let's go break another commodity market.

- Jack

I appreciate reader feedback, so if you enjoyed today’s piece, let me know with a like or comment at the bottom of this page!

Young Money is now an ad-free, reader-supported publication. This structure has created a better experience for both the reader and the writer, and it allows me to focus on producing good work instead of managing ad placements. In addition to helping support my newsletter, paid subscribers get access to additional content, including Q&As, book reviews, and more. If you’re a long-time reader who would like to further support Young Money, you can do so by clicking below. Thanks!

Sources:

The Essex Boys: How Nine Traders Hit a Gusher With Negative Oil

Detailed analysis on The Bank of China's poor risk management

An oil futures contract expiring Tuesday went negative in bizarre move showing a demand collapse

China's 'Crude Oil Treasure' Promised Riches. Now Investors Owe the Bank.

Story of mysterious traders who made over $600M in one day when oil went negative

Jack's Picks

My friend Alex Banks has a great VC/investing/startup podcast called "Through the Noise." A couple of weeks ago, he hosted Jamin Ball, a partner at Altimeter Capital, to discuss shifts in SaaS and the tech landscape. Check it out here!

Morgan Housel's latest piece on assets coming back to reality is great, give it a read here!